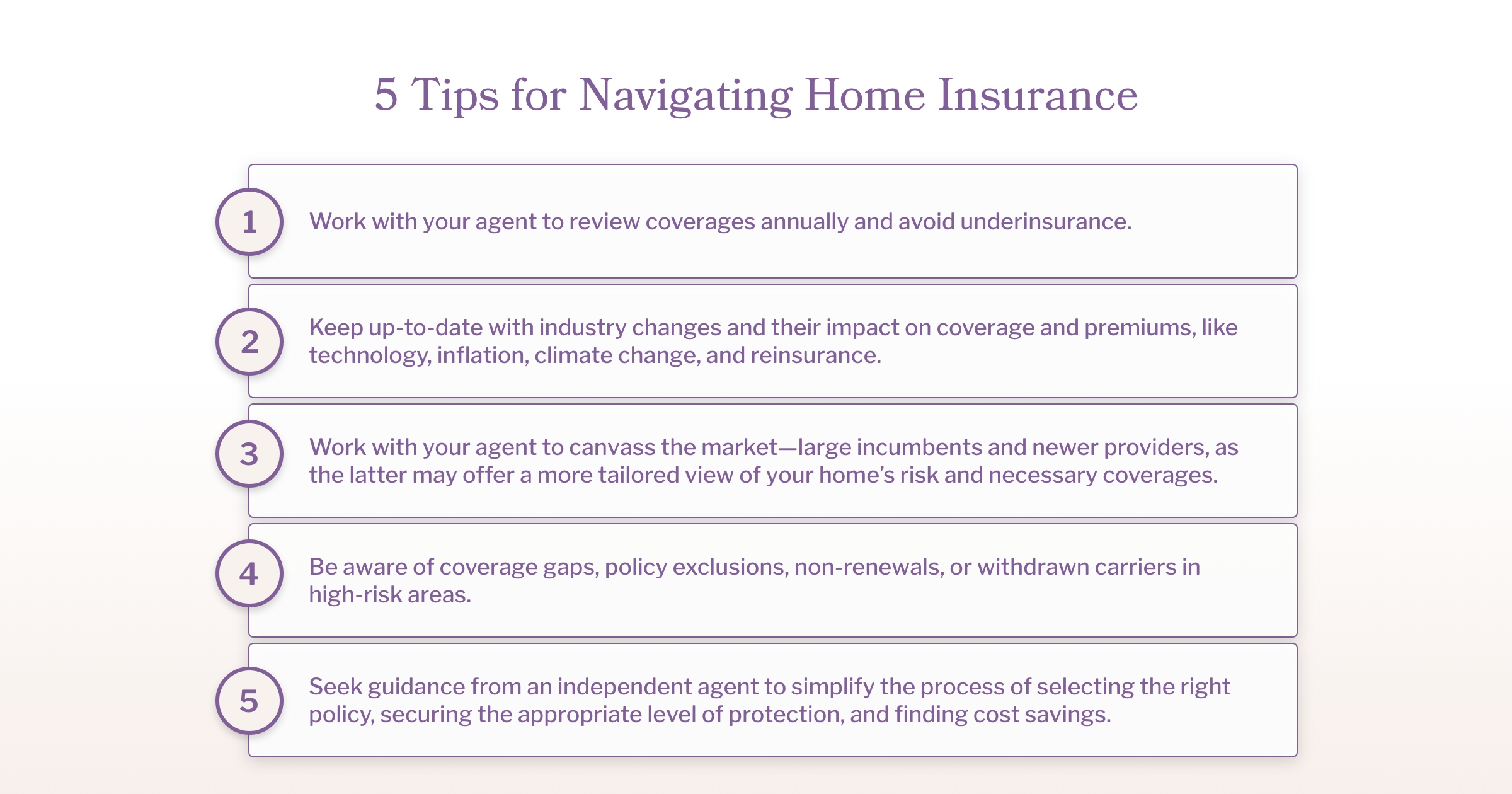

The insurance industry is facing a myriad of challenges including inflation, the effects of climate change, and restrictions imposed by reinsurers. These factors are significantly impacting the industry and may continue well into the future.

However, with these challenges comes opportunity. Niche carriers have the opportunity to own a piece of the pie, with ample opportunity to leverage new technologies, data analytics, and more sustainable business practices. Because of this, the industry is positioned to ensure policyholders continue to have access to the insurance coverage they need.

The intersection of technology, inflation, climate and reinsurance

J.D. Power found the majority of homeowners—52%—don’t fully understand their coverage.1 So when it comes to comprehending home insurance, the best place to start may lie in understanding the latest factors impacting the industry—for better or worse.

Advancements in technology, including the use of increasingly sophisticated predictive analytics, are helping insurers better understand and mitigate risks. Insurers are beginning to use artificial intelligence and big data to more accurately assess risk and price policies. By analyzing data regarding a property’s age, location, and condition, insurers are more accurately predicting the likelihood of a claim and are pricing their policies accordingly, leading to more tailored coverage options for consumers.

Despite, or perhaps in part due to the use of technology and data in determining insurance rates, the cost of home insurance has risen dramatically over the last 12 months. While inflation has risen by 8.3%, insurance premiums have outpaced inflation and increased (on average) by 12.1%, up to 18.5% in certain states.2 This can partially be attributed to inflation and the increased cost of construction materials. As the cost of goods and services increases, insurers are forced to raise premiums to keep pace with rising costs.

To put it simply, just as inflation impacts premiums, claims, and payouts, the rising cost of construction materials impacts the cost of rebuilds.

Adding to the increased cost of rebuilds and compounding rate increases, is the increase in weather-related losses. As the frequency and severity of natural disasters increases, so too does the risk of damage. The increase in catastrophic weather events strains not only homeowners, but insurers as well.

Many homeowners are facing higher premiums and in extreme cases, canceled policies or the complete withdrawal of carriers in their market due to increased risks—and tightened restrictions by reinsurers. 50 years ago, there was less risk simply because the population was dispersed elsewhere. Due to urban sprawl, population growth, and shifting populations, homeowners in regions prone to natural disasters are seeing more—and greater—losses. And reinsurers are seeing it, too.

Balancing risk and adapting to changing demand

Reinsurance is insurance for insurance companies. It's a way to distribute and minimize risk following catastrophic events. Insurers themselves don't want sole ownership of these risks because they often cost more than average premiums would cover, and it’s a logical decision to share this burden with larger entities.

Moody’s found that more than 70% of wildfire losses between 1980 and 2018 occurred between 2016 and 2018 alone.3 The uptick in claims frequency and payout amounts increase has subsequently caused reinsurance to be at its most expensive in 30 years.

Reinsurers are not only tightening restrictions to remain profitable, but they’re also raising costs for insurers, which carriers then pass on to policyholders. In extreme cases, carriers are even pulling out of some markets entirely, like Florida or other coastal regions. Homeowners are then left with non-renewed policies and scrambling to secure coverage from the remaining number of carriers in their market; carriers who are often ill-equipped to accommodate the increase in claims related to weather events or other natural disasters.

Fortunately, newer insurance providers are helping fill the void left by these legacy carriers.

Coverage review and expert advice is crucial for a secure future

Because of inflation, climate change, and new restrictions affecting insurance carriers and homeowners alike, being underinsured has become endemic among homeowners. In fact, it is so rampant among homeowners, that an estimated 60% of policyholders have undervalued the replacement cost value of their home by an average of 17%.4

Being underinsured means having less coverage than needed to cover the cost of rebuilding a home or replacing belongings following a loss.

There have always been coverage gaps and policy exclusions, such as is the case with floods or earthquake coverage. And while there are subtle differences in policy terms, some insurers will cover things that other insurers won’t. Simply put, some policies and insurers are more generous than others, however.

But when people start out underinsured, and then inflation occurs, homeowners can find themselves lacking the protections they require. Homeowners renovate their homes, buy more furnishings and belongings, and don’t think about increasing their insurance coverage. In fact, coverage is often not questioned—until disaster strikes. The onus is on the policyholder to review coverage annually and ensure they are protected for all the right things.

One way homeowners can ensure they’re protected with an appropriate level of coverage is by seeking expert advice and working with an independent agent. Coverage is complicated enough; independent agents can guide homeowners to understand their options, find savings, and secure the right level of coverage.

Confronting the challenges of home insurance

Is it more complicated than it used to be to insure a home? There’s a lot more to it, that’s for certain. Carriers now know more about the home and quote policies based on more variables. They can look at photos of the house to determine roof coverage, and factors like claiming history and home age matter more than they used to.

Although only 6% of policyholders filed a claim in 2020, the cost of property claims is expensive and only continues to rise, with losses trending north, in both frequency and severity.5 There are coverage features homeowners can look for to protect themselves in the event of a loss, including buffering policies with replacement cost coverage and sub-coverages, and ensuring adequate coverage for additional living expenses. While it’s critical that homeowners understand insurance policies and coverages, it is equally important that the insurance industry adapts to changing environments.

1 J.D. Power. “Satisfaction with home insurance faces critical test as hurricane losses mount, J.D. Power finds.” 18 September 2017. Accessed 30 January 2023. https://www.jdpower.com/business/press-releases/jd-power-2017-us-home-insurance-study

2 Ryan Ermey. “The 10 States where home insurance rates are rising the fastest—and none are New York or California.” CNBC. 6 October 2022. Accessed 2 February 2023. https://www.cnbc.com/2022/10/06/states-where-home-insurance-rates-are-rising-fastest.html#:~:text=Arkansas'%20pace%2Dsetting%20increase%20amounts,than%20they%20did%20in%202021

3 John Rees. “Reinsurance Outlook Stable, but Climate Change Risks Rising, Moody’s Says.” SP Global. 3 September 2019. Accessed 6 February 2023. https://www.spglobal.com/marketintelligence/en/news-insights/trending/6iJWX3OnZpLAMEoaBALUqQ2

4 Claims Journal. “Insurance industry’s property undervaluation issue continues to improve.” MSB. 8 August 2013. Accessed 26 January 2023. https://www.claimsjournal.com/news/national/2013/08/08/234498.htm

5 Insurance Information Institute. “Facts + Statistics: Homeowners and renters insurance.” 2022. Accessed 23 January 2023. https://www.iii.org/fact-statistic/facts-statistics-homeowners-and-renters-insurance